What Is EPT

Every vToken in a series splits into: One side wants principal + yield exposure and gives up the rewards side. The other side pays upfront and holds the rewards side through EPT. EPT accrues credits while you hold it. Your credit share determines how many CreditTokens you can claim for each period. EPT trades on the EPT/vToken orderbook. You buy EPT for a small upfront price because you are only buying the rewards side, not the principal + yield side. See Orderbook Guide for how to reason about APR and place EPT orders in the app.Credits

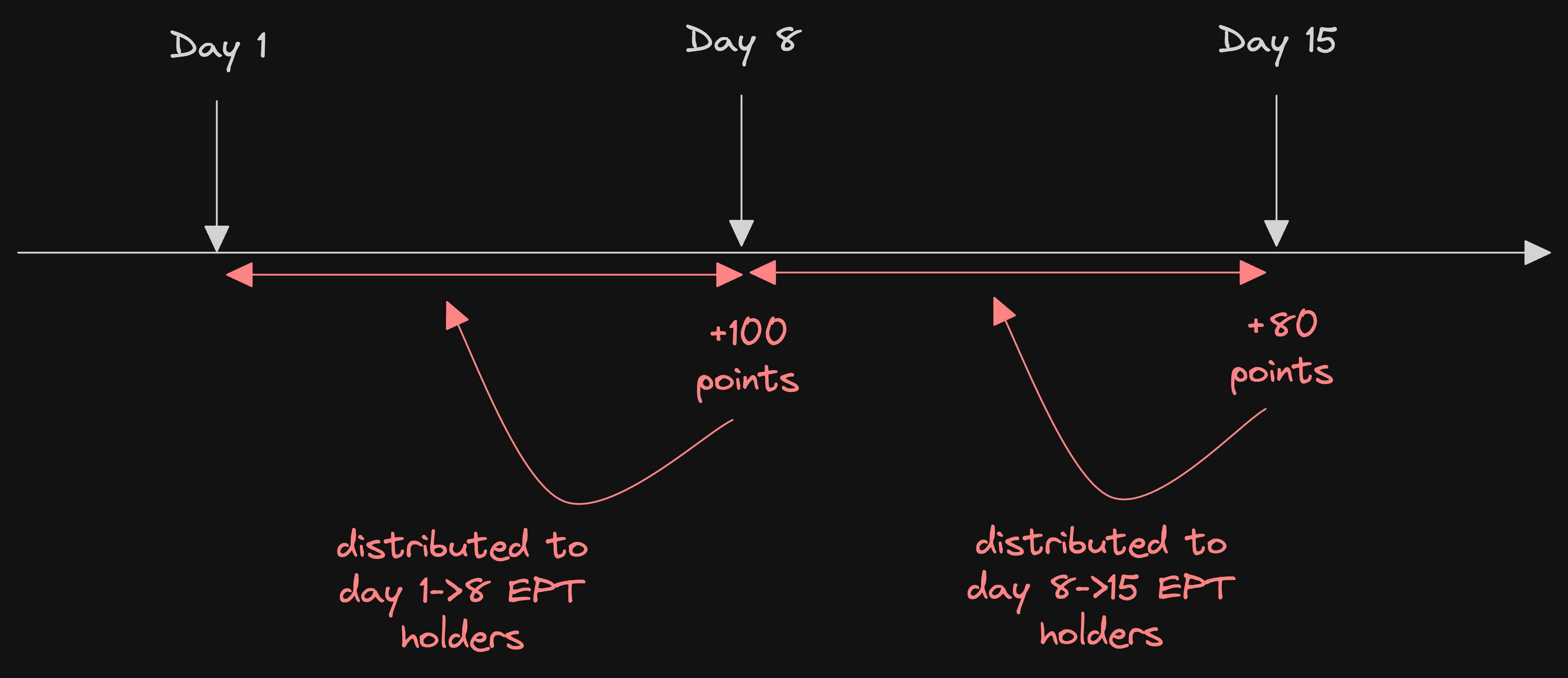

EPT accrues credits while you hold it — the longer you hold and the more you hold, the bigger your share of CreditTokens. Credits are tracked automatically on-chain. Fresh start. When you buy EPT, your credit counter starts from zero. The seller keeps their accumulated credits. No credit inheritance. Hold earlier, earn more. Earlier credit periods are locked in, so later buyers do not dilute earlier holders.

Buy the Rewards Side

ST buyers give up the rewards side for principal + yield exposure. That leaves EPT available at a low upfront price because it only represents the rewards side. Example. EPT trades at $0.02. That means for the cost of 1 vToken, you can buy 50 EPT.- Price per EPT: $0.02

- EPT bought with 1 vToken: 1 / 0.02 = 50 EPT

- Rewards-side exposure scales with how many EPT you can hold for the same upfront cost